⸺Do Business in Thailand⸺

Taxes in Thailand

Taxes in Thailand

Value Added Tax (VAT)

The “Value Added Tax (‘VAT’) is a tax on the sale of goods or the provision of services. The current rates are 7% and 0% (on export activities for instance) while some exemptions apply to certain activities.

Tax Invoice

A tax invoice is a mandatory document that needs to be issued by sellers of goods and services in order to submit VAT.

Withholding Tax (WHT)

The withholding tax (“WHT”) is a tax deducted at source from the payment of a service invoice. WHT rates depend on the nature of provided services (cf. below detailed rates).

Personal Income Tax (PIT)

The Personal Income Tax (PIT) is a direct tax levied on the income of taxable persons, i.e individuals residing in Thailand more than 180 days in a calendar year, or non-resident earning income in Thailand.

Corporate Income Tax (CIT)

The CIT therefore applies to entities incorporated under Thai law, as well as to foreign entities conducting business in Thailand or receiving income paid from or in Thailand which is subject to CIT under the Thai Revenue Code.

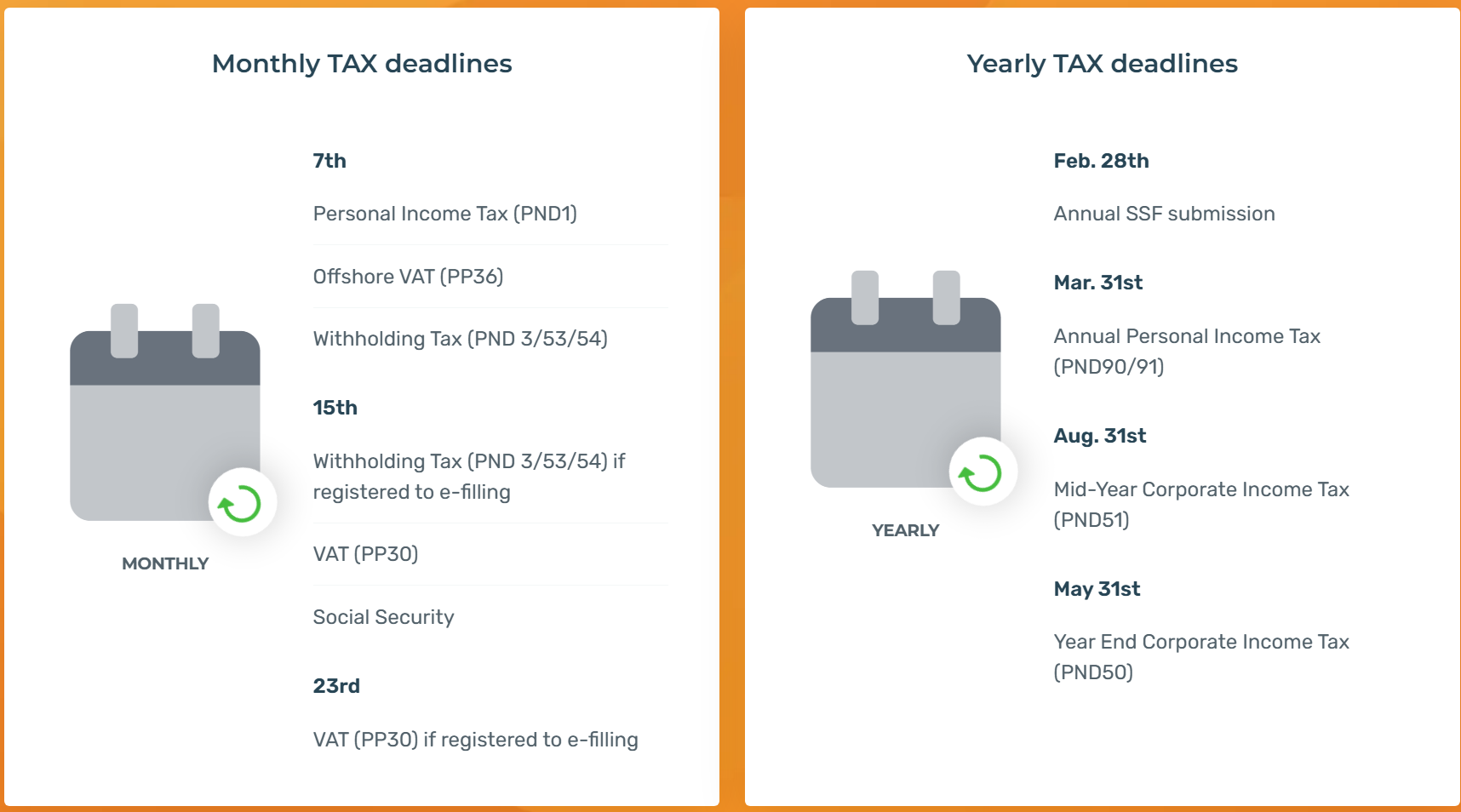

Tax Deadlines in Thailand